June 17, 2020

In this special report, Slingshot has teamed up with AMIN partner agency DPR&Co of Australia to analyze the implications of emerging trends in the Asia/Pacific region.

Could anyone have ever seen the panic buying of toilet paper coming in the early phases of the COVID-19 pandemic? Or what about the massive surge in online grocery sales? If they were paying attention to what was happening in Asia, yes they could.

With the pandemic impacting countries in the Asia Pacific region months before the U.S., trend watchers in North America, Europe, and elsewhere were able to observe how consumers and brands alike reacted, and then forecast behavior related to their own countries.

Mintel has released a comprehensive report on the current state of the consumer experience in the Asia Pacific region. Now, as we move squarely into the phased easing of lockdowns, it is again wise to look to the APAC region as a bellwether, as it has already passed through the same phases we’re moving into right now, showing us what we can expect here at home.

It should be noted that the COVID experience is far from uniform across the region. According to Phil Huzzard, Principal at Melbourne-based DPR&Co, countries such as Indonesia, India, Bangladesh, Pakistan, the Philippines and even Singapore are still dealing with relatively high infection rates. In some of these countries, there is also doubt as to the effectiveness of infection tracking and reporting.

China, New Zealand, Malaysia and Australia have found themselves at single digit infection rates, but these situations remain fluid and may change from one week to the next.

There are also significant cultural differences between these countries, so their response to the recovery has shown up in different ways. Mask-wearing, for example, is almost non-existent in New Zealand and Australia, but still widespread in China.

With all of this in mind, here are six trends from the Asian experience that will likely matter to U.S. marketers:

Easing the lockdown will equal less panic buying.

Toilet paper and eggs for everyone! It was clear that the rapid move to a state of lockdown this past spring created widespread panic among American consumers, leading to panic buying and empty shelves in supermarkets.

“In Asia, the beginning of the pandemic was marked with panic buying of everything non-perishable – canned foods, rice, legumes – as well as a surge on staples such as bread, milk and paper products, such as toilet paper and paper hand towels,” Huzzard says.

But just as it has happened in the Asia Pacific region, we can expect panic buying to quickly abate, with supermarkets once again able to keep staples on the shelf throughout the day. Currently, only about 9% of APAC shoppers still feel the impact of panic buying on their own shopping experiences.

“This was over very quickly once the infection rate began to slow,” Huzzard adds, indicating that in markets where the recovery is well advanced, there are no product shortages in any category. In addition, major retailers in some countries have even gone public in their refusal to take back products bought in panic.

It’s possible that in the U.S. and elsewhere, we’ll see a glut of certain products, as that same trend of panic buying left many households with supplies that will last them for weeks or even months.

Brands should look at in-store social distancing as a long-term strategy.

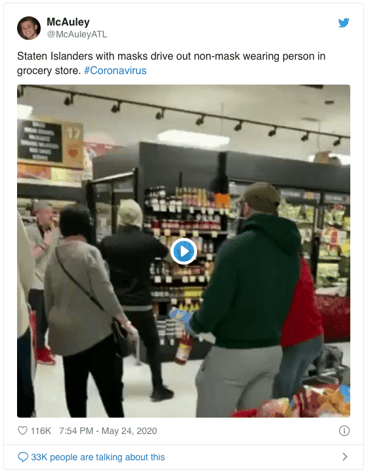

Staten Islanders have been quite vocal in their desire to get life back to normal. But as a recent video of angry shoppers showed us, they are also determined to stay safe even as restrictions are lifted. This is the balance most Americans will seek – between normalcy and safety as COVID-19 cases continue to surge in many parts of the country.

In some countries within the APAC region, retailers have met similar expectations by treating social distancing and safety measures as long-term strategies. 90% of stores continue to offer free hand sanitizer to customers, 85% have maintained social distancing measures (although the policing of them has been inconsistent), and 80% require customers to wear masks– except in Australia and NZ where mask-wearing is under 30% and never mandated except in circumstances where there are immune-suppressed people. Temperature checks and protective barriers at the register have also become the norm in some countries.

Meanwhile, the low infection rates in countries such as New Zealand and Australia have led to some complacency on the part of many shoppers, particularly in the garden/home improvement and grocery sectors, with crowds approaching pre-COVID levels.

Restauranteurs show continuing strong take-out and home delivery demand, although this is changing as a gradual return to in-restaurant dining gathers momentum.

It is clear that there is a strong direct correlation between success in reducing infection rates and a relaxation of public attitudes toward personal exposure. Though the current U.S. political climate will likely keep some of these measures from fully establishing themselves from coast to coast, we can expect consumers in more densely populated urban centers to expect and demand them so long as COVID-19 cases continue to rise.

Less stress on online sales will lead to a better consumer experience.

Americans have flocked to online grocery platforms in incredible numbers over the past several months, and as we’ve mentioned in previous posts, this behavior is likely to continue over the long haul. That’s not only good news for online channels such as Amazon and Instacart, but for the CPG brands that have invested in ensuring their products are top-of-mind for online shoppers.

But perhaps more important is that we can expect the stresses on these still-maturing platforms to ease in the coming months. In APAC, this has meant shorter wait times for customers, more products in stock, and faster, more accurate fulfillment. In other words, a better customer experience which has in turn meant less customer churn, with more people sticking with their online grocery buying behavior. In the U.S., we can expect the same.

Retail live streaming will continue to surge in popularity.

Lazada may be a relatively unknown brand in North America, but it’s currently the leading e-commerce platform in Southeast Asia. Lazada saw a massive uptick in live stream shopping during the lockdown, with 70 times more streams between shoppers and retailers.

Lazada’s Shopee Live Stream service is especially popular in Malaysia, with a current average of over three million daily direct messages between buyers and sellers. Live streaming was already on an accelerated growth curve in Asia prior to the lockdown, and COVID-19 only added fuel to the fire. While live streaming has not taken off as widely thus far in the U.S., leading brands are catching on, and we can expect young, digitally-driven shoppers here to drive growth in this channel even as the lockdown eases.

“Big ticket” online sales will continue to rise.

It’s no accident that U.S. television viewers are seeing more ads from online car buying services like Carvana and Vroom. Vroom, in particular, seemed to emerge on the scene out of nowhere. The VC-backed car site rapidly grew awareness at a time when car shoppers were mostly staying home and looking for bargains in the used market. And judging from its IPO, Wall Street is bullish on its future, with a $5.4 billion valuation after its first day of trading.

This mirrors the trends coming out of APAC as well, and even the car brands themselves are getting into the act. Toyota, for example, has established its own branded Lazada e-store to offer vehicles directly to shoppers who prefer to stay home.

DPR&Co’s Huzzard reports that vehicle sales have spiked significantly in a number of APAC countries (especially Australia), as have sales of caravans. This is attributed to forced savings from COVID over the past 2 months as well as the large-scale cancellation of international recreational travel. The faster than anticipated recovery has also lifted consumer confidence somewhat, although this may be moderated as countries pull back on stimulus measures and the full effects of the economic shock is felt by the business community.

Other big-ticket items are being purchased in the digital space as well, with Malaysian property developers like Sunway moving over $40 million worth of real estate online in April alone—just as the lockdown was easing.

Brands offer support to low income households still out of work.

Across APAC, it was the poorest households who felt the most financial pain as a result of the lockdown. Just like in the West, retail, restaurant, hospitality, and other service jobs disappeared virtually overnight. But will take much longer to bring those jobs back, both in Asia and here at home.

Grocery brands in APAC have responded with stepped up support for food banks and pantries. In some cases, they’re even changing store policies to offer direct assistance. In Thailand, for example, supermarket brand Tesco Lotus is providing free food and essentials to people in need directly from multiple store locations. And in rural parts of the country, “convenience sharing” stores have been set up, where people in need can choose up to five free items once a week. Other countries, meanwhile, have stepped up the distribution through NGOs of perishables approaching their use-by dates.

Similarly, U.S. food and grocery brands should be thinking of ways to help the millions of Americans still out of work. As we’ve discussed in other recent posts, showing purpose and actively helping to create solutions should be top of mind for every brand right now. Now’s the time for brands to show they care, putting their products and services to work for the greater good.

***

While cultural differences will no doubt lead to variations on how certain shopping trends are adapted in North America and other regions, we know from past experience that many consumer habits are driven largely by human behavior that transcends culture. And many of the emerging trends we continue to see here at home, such as live streaming, find their roots firmly established in other parts of the world.